This company offers a compelling case of asymmetric returns

$OSCR

This company offers a compelling case of asymmetric returns.

First, I’m not a healthcare policy expert. The only reason this company came onto my radar is because of Oguz Erkan, whose writing I follow on Substack. Rather than repeat his excellent introduction, I encourage you to read his original piece here: Oscar Health: A 100-Bagger in the Making.

What caught my attention is how uncertainty seems to have disproportionately punished the stock, even when considering downside risks.

Let’s address the bear case head-on. I don’t have a crystal ball, and frankly, I doubt even Trump knows what he’d do on this front. So let’s start with the worst-case scenario: a full repeal of the ACA.

The Affordable Care Act (ACA), also known as Obamacare, is a landmark U.S. law signed in 2010 to expand access to affordable health insurance. As of 2025, over 40 million Americans rely on ACA-related coverage, including Marketplace plans, Medicaid expansion, and young adults on family insurance — that’s more than 1 in 8 Americans.

The ACA has grown increasingly popular over time. Recent polls show that around 60% of Americans support keeping or expanding it. In both the 2022 and 2024 midterms, Democrats campaigned aggressively on protecting the ACA. Even the Republican stance has evolved — from full opposition to implicit acceptance, as many red states now benefit from ACA-related programs like Medicaid expansion.

Given the political landscape and ACA’s deep integration into the healthcare system, I believe there’s less than a 10% chance it gets repealed outright.

Worst Case: ACA Fully Repealed (10% Probability)

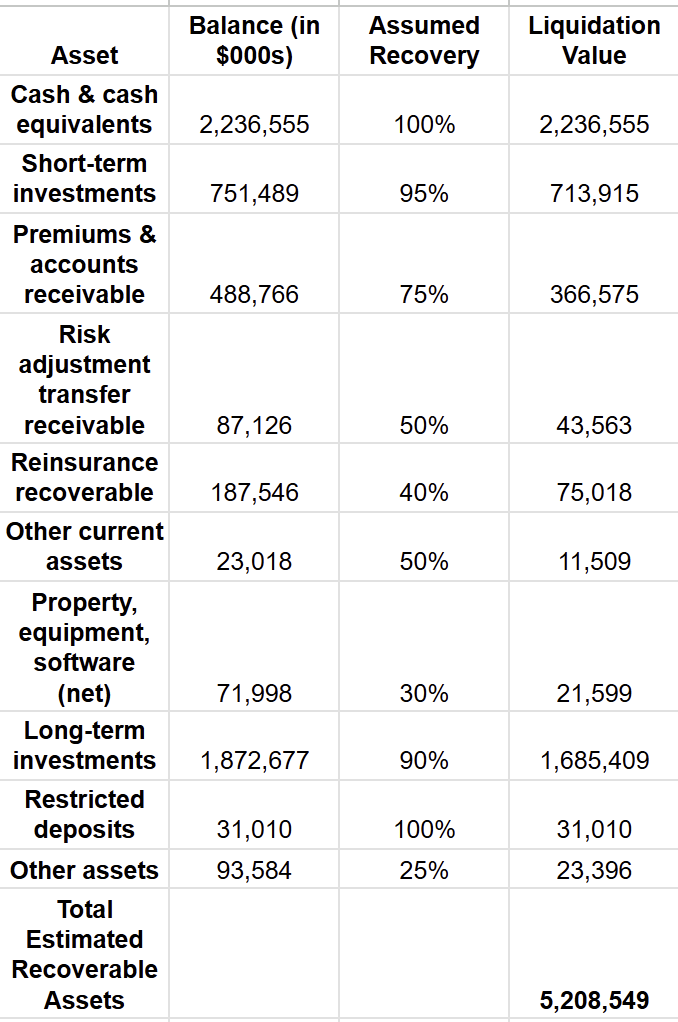

This scenario would be disastrous for shareholders. Without the ACA, Oscar’s core business model — individual and family plans sold through the Marketplace — becomes unsustainable. The company would likely be sold off or liquidated.

Let’s estimate its liquidation value:

Estimated Realizable Assets (conservatively): $5,208,549,000

Total Liabilities: $4,507,654,000

Net Liquidation Value: 5,208,549−4,507,654=700,895 (in thousands) or $2.77 per share.

Base Case: ACA Intact, No Subsidy Extension (50% Probability)

Oscar’s management has guided for ~20% compound annual revenue growth and ~5% operating margin by 2027, even assuming enhanced subsidies are not extended (source).

Let’s quantify that:

2025 Revenue: $9.2 billion

2027 Revenue (20% CAGR):

9.2×(1.2)^2 = 13.25 billionOperating Income (5% margin):

13.25×5%=662.5 millionNet Income (20% tax):

662.5×80%=530 millionImplied Market Cap (at 15× P/E):

530×15=7.95 billion or $31.36 per share

Bull Case: Subsidies Extended (40% Probability)

In this scenario, Congress passes a subsidy extension, maintaining enhanced financial support for ACA Marketplace enrollees.

Revenue CAGR: 22%

Operating margin: 7%

Tax rate: 20%

P/E multiple: 20×

2027 Revenue (22% CAGR):

9.2×(1.22)^2 = 13.7 billionOperating Income (7% margin):

13.7×7%=959 millionNet Income (20% tax):

959 ×80%=767 millionImplied Market Cap (at 20× P/E):

767×20=15.3 billion or $60 per share

Putting it all together:

The expected share price can be calculated using a probability-weighted average:

Expected Share Price=(0.10×2.77)+(0.50×31.36)+(0.40×60)=40

Based on this, the probability-weighted average share price is approximately $40.

Starting from today's price of $16.56, this implies a compound annual growth rate (CAGR) of 33% over 3 years — a highly attractive return.

However, given that there remains a 10% chance of downside to $2.77, it’s essential to size your position thoughtfully.

Disclosures: I am long $OSCR . The information contained in this article is for informational purposes only. You should not construe any such information as legal, tax, investment, financial, or other advice. None of the information in this article constitutes a solicitation, recommendation, endorsement, or offer by the author, its affiliates, or any related third-party provider to buy or sell any securities or other financial instruments in any jurisdiction in which such solicitation, recommendation, endorsement, or offer would be unlawful under the securities laws of such jurisdiction.